If you are running a business, the annual Workers’ Compensation audit is likely right up there with a dental root canal on your list of favorite activities.

Every year, the process plays out the same way: an auditor reviews your actual books from the prior year, compares them to the estimates you provided at renewal, and sends you a bill. For far too many business owners, that final audit results in a massive, unbudgeted “catch-up” premium that hits their cash flow like a sledgehammer.

At Skyscraper Insurance, we look at this process differently. A surprise audit bill isn’t just bad luck—it’s a sign of a broken mid-year strategy.

As we cross the mid-year mark, your payroll realities have almost certainly shifted from the projections you made six months ago. If you aren’t auditing your own data right now, you are setting yourself up for an aggressive surprise at the end of the year. Here is how to execute a mid-year check and take control of your numbers before the auditor arrives.

1. The Proportional Premium Trap

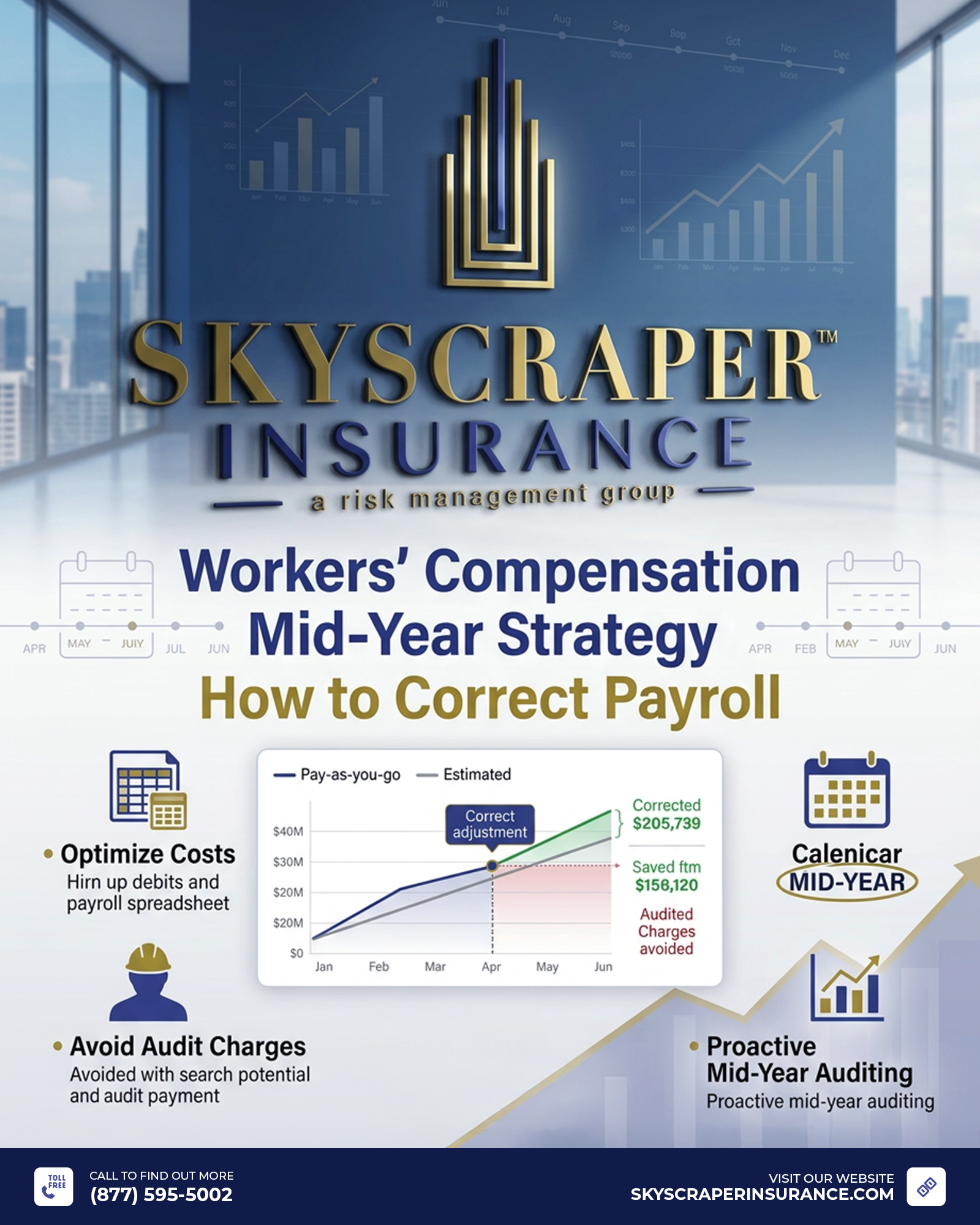

When you set up a traditional Workers’ Comp policy, your premium is based on an estimate of your annual payroll. The insurance carrier takes that total figure, applies your specific class code rates, and divides it into equal monthly payments.

The problem is that business isn’t static.

If you projected a payroll of $1,000,000 at renewal, but your business experienced rapid growth, your actual numbers might be tracking toward $1,500,000. The carrier isn’t charging you for that extra $500,000 during the year. Instead, that liability is quietly building up in the background.

When the year-end audit occurs, the carrier will demand the entire premium for that missing $500,000 all at once.

Conversely, if your payroll shrunk because you downsized or lost a contract, you are effectively overpaying the carrier every single month—giving them an interest-free loan with cash that should be funding your operations.

2. Class Code Drift: The Costliest Audit Mistake

Payroll volume is only half the battle; where that payroll is allocated matters just as much. Underwriters use four-digit classification codes to determine the risk level of your employees.

During a mid-year hiring surge, it is incredibly easy for “class code drift” to occur.

The Cost of Misclassification:

Let’s say you hire a new employee to handle basic clerical work ($Class\ Code\ 8810$, which carries a low rate of perhaps $0.25$ per $\$100$ of payroll).

If your payroll manager accidentally drops them into a general light-manufacturing code ($Class\ Code\ 3632$, which might cost $3.50$ per $\$100$), you are overpaying by thousands of dollars.

Even worse, if a supervisor moves a field laborer into a light warehouse role but fails to update their operational code, an auditor will default the entire employee’s wages to the highest-risk category.

The Payroll Adjustment Matrix: Projections vs. Reality

To help your finance team identify where your audit vulnerabilities sit, look at how common mid-year operational shifts change your final audit outcome:

| Operational Shift | The Unmanaged Impact | The Proactive Correction | Audit Outcome |

| Headcount Growth (+20%) | Liability accumulates quietly for 12 months. | Report the trend mid-year; adjust the baseline projection. | Clean Audit: Incremental, manageable monthly premium changes. |

| Using Uninsured Subcontractors | Contractor payments are swept into your audit. | Collect valid Certificates of Insurance (COIs) before cutting checks. | Saved Capital: Avoids paying Workers’ Comp premiums on independent teams. |

| Executive Officer Exclusion | Officers are automatically included by default. | File formal exclusion waivers with the state rating bureau. | Lower Premiums: Strips high-executive salaries out of the rate calculation. |

| Bonus / Overtime Spikes | Gross overtime wages are taxed at full standard rates. | Track and separate the “overtime premium” (the extra half-time pay) in your logs. | Audit Discount: Auditors must deduct the premium portion if clearly broken out. |

3. The Myth of the “Pay-As-You-Go” Cure

Many businesses switch to “Pay-As-You-Go” workers’ comp programs to avoid audit surprises. These programs tie your premium directly to your real-time payroll submissions every pay period.

While Pay-As-You-Go is excellent for managing cash flow volume, it is not a magic bullet for class code accuracy.

If your team enters an employee under the wrong classification code in January, the system will accurately calculate the wrong premium every single week. When the auditor shows up at year-end, they will still reclassify those employees and hand you a retroactive bill. Software cannot replace active operational oversight.

Take Control: Schedule Your Mid-Year Payroll Reconciliation

You shouldn’t have to guess what your insurance will cost at the end of the year. True cost control isn’t about hoping your estimates were right; it’s about actively adjusting your policies to match the real-world trajectory of your business.

At Skyscraper Insurance, we practice continuous risk management. We don’t believe in waiting for an auditor to grade your paperwork. Our dedicated risk advisors work alongside your accounting team mid-year to run true payroll checks. We review your class code distributions, audit your subcontractor certificates, isolate your overtime data, and realign your policy projections so you can face your next renewal with absolute financial certainty.

Are your current payroll estimates protecting your cash flow, or are they hiding a massive year-end bill?

Don’t let a clerical estimate write an unbudgeted check against your profit margins. Reach out to our expert commercial advisory team today for a comprehensive Payroll reconciliation. We will align your policy data with your current operations, eliminate class code drift, and ensure your business stays completely protected without the year-end surprises.