If you own commercial real estate, you likely check your property’s market value with a mix of pride and strategy. You know exactly what the building down the street sold for last quarter, and you know what your portfolio is worth on paper.

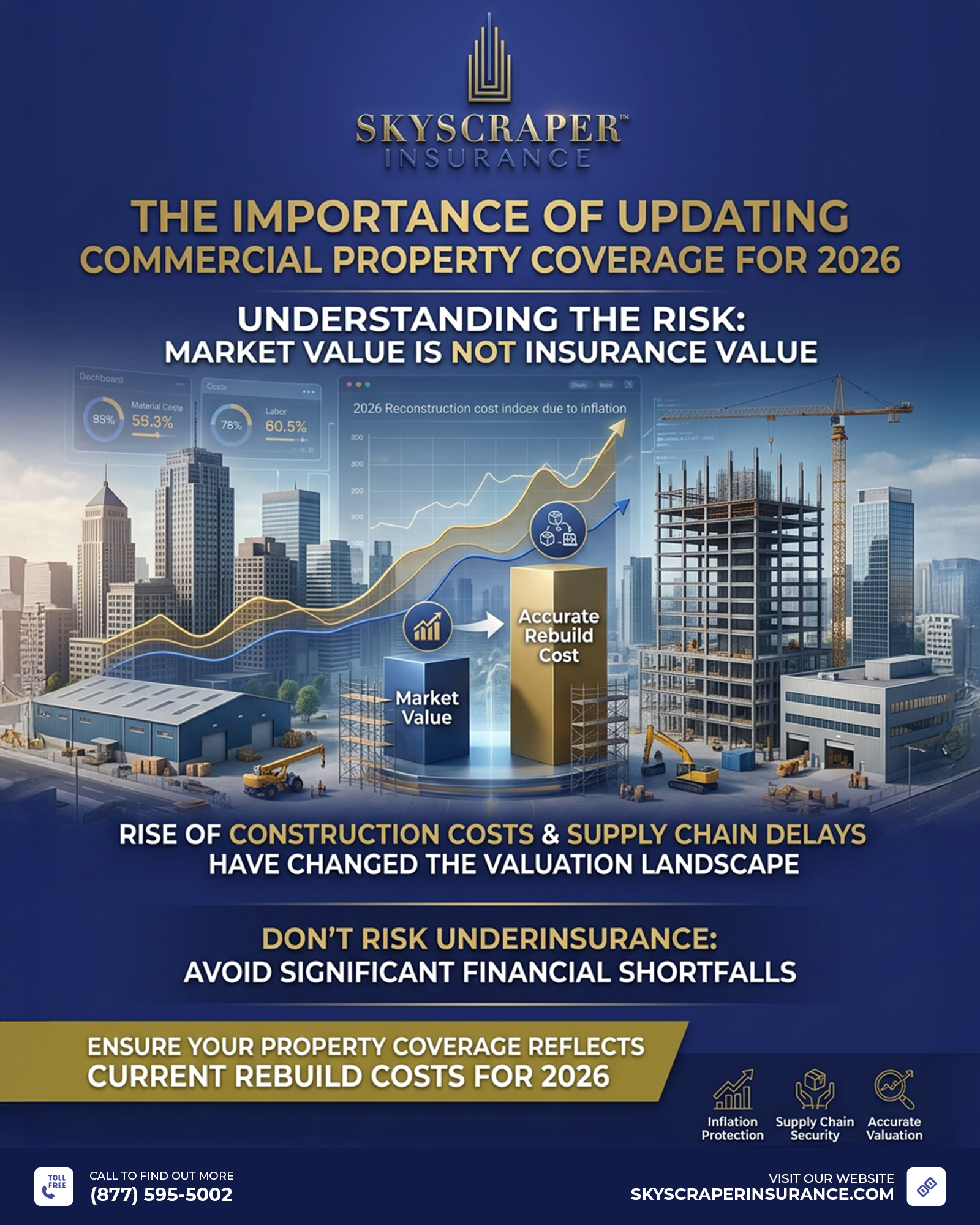

But here is a critical real estate reality check for 2026: Market value has absolutely nothing to do with insurance value.

At Skyscraper Insurance, we are witnessing a quiet crisis across the real estate sector. Property owners are flying blind, relying on property valuations that are two, three, or even five years old. In 2026, lingering supply chain friction, specialized labor shortages, and years of compounded inflation have driven reconstruction costs to historic highs.

If you haven’t adjusted your property coverage recently, you are likely suffering from inflation-driven underinsurance—meaning you are paying premiums for a safety net that will rip the moment a catastrophic claim hits.

1. The Anatomy of the Rebuild Gap

The root of the problem lies in the difference between what someone will pay to buy your building versus what a contractor will charge to rebuild it from the ground up after a total fire or structural collapse.

When a disaster occurs, you aren’t just paying for new drywall and studs. You are paying for:

- Demolition and Debris Removal: Clearing a ruined site in 2026 requires specialized hazardous waste disposal and eco-compliance, which have spiked in cost.

- Up-to-Code Enforcement: If your building was built in 1995, you cannot rebuild it to 1995 standards. Local municipalities will mandate modern energy-efficiency, ADA compliance, and advanced fire-suppression systems.

- The Labor Premium: Trade labor shortages haven’t eased. Standard general liability rates for contractors have risen, and those costs are passed directly to you in a reconstruction bid.

2. The Coinsurance Trap: A Hidden Financial Penalty

Many owners assume that if they have a $2 million policy on a building that costs $3 million to rebuild, they are at least safe for any “partial” loss up to $2 million.

This assumption is entirely wrong.

Most commercial property policies contain a Coinsurance Clause (typically 80% or 90%). This clause mandates that you must carry insurance equal to a specific percentage of the building’s actual replacement value. If you fail to meet that threshold, the insurance carrier applies a proportional penalty to your claim—even for small, partial losses.

The Underinsurance Penalty in Action:

Let’s say your building’s true 2026 replacement cost is $5,000,000.

With an 80% coinsurance clause, you are required to insure it for at least $4,000,000.

If you kept your old policy limit of $2,000,000, you are only carrying 50% of the required insurance.

If a kitchen fire causes $200,000 in damage, the carrier will not pay the full $200,000. They will pay 50% of the loss minus your deductible. You end up holding a bill for $100,000 out of pocket for a minor claim.

Market Value vs. Rebuild Cost: The 2026 Reality

To understand where your vulnerabilities lie, review the fundamental divergence between these two valuation methods:

| Valuation Metric | Market Value | Rebuild (Replacement) Cost |

| Driven By | Buyer demand, location, interest rates, and land value. | Cost of raw materials, trade labor, fuel, and local building codes. |

| Includes Land? | Yes (often a massive portion of the asset value). | No (the dirt doesn’t burn down). |

| 2026 Trend | Stabilizing or fluctuating based on economic policy. | Sustained upward trajectory due to sticky material prices. |

| Worst-Case Threat | Market downturn / loss of equity. | Coinsurance penalties and massive out-of-pocket shortfalls. |

3. The “Ordinance or Law” Blindspot

Even if you get the base replacement cost right, a standard property policy only covers putting the building back exactly how it was before the loss.

In 2026, environmental and structural regulations are shifting rapidly. If your roof is destroyed, new green building codes might mandate solar-ready infrastructure or specific insulation values that cost an extra 25%. Without a robust Ordinance or Law endorsement tied to an updated property valuation, those regulatory upgrades will come directly out of your operating capital.

Take Control: Update Your Replacement Values Today

Relying on old valuations in today’s economic climate isn’t just an oversight—it is a threat to your business continuity. A major loss shouldn’t be the event that reveals your insurance policy is out of date.

At Skyscraper Insurance, we don’t believe in guesswork. Our dedicated risk advisors utilize advanced forensic valuation tools to calculate the precise, real-time reconstruction costs for your specific asset class and zip code. We help you eliminate the risk of coinsurance penalties, secure critical Ordinance or Law protections, and ensure your premium dollars are actually buying the security you expect.

Is your portfolio truly protected, or are you carrying tomorrow’s liabilities on yesterday’s numbers?

Don’t wait for a catastrophic claim to expose the gap. Reach out to our expert team today to update replacement values and fortify your real estate investments against inflation.