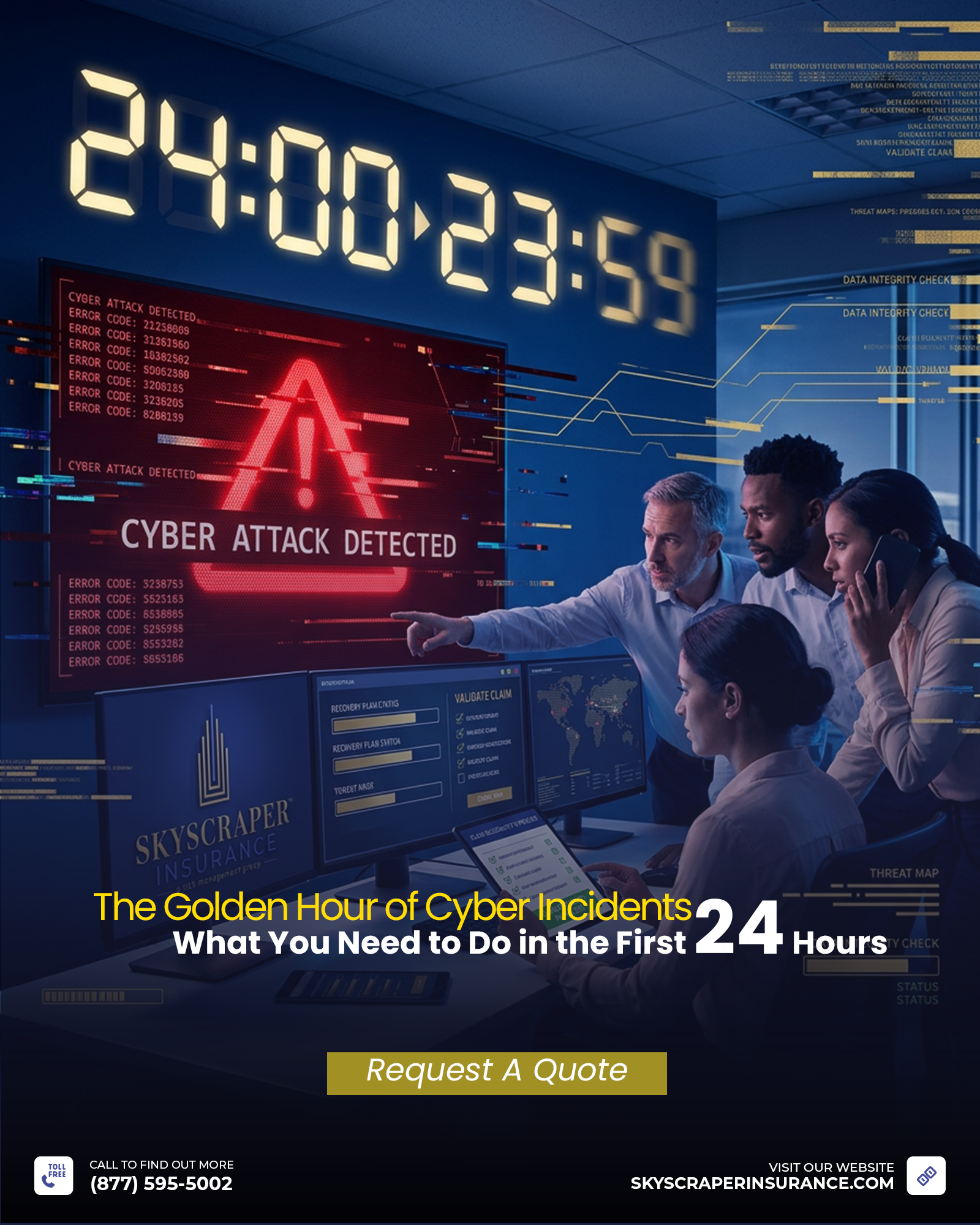

In the world of cyber insurance, the first 24 hours after a suspected breach is often referred to as the “Golden Hour.” It is the window where the trajectory of your recovery—and the validity of your insurance claim, is decided.

At Skyscraper Insurance, we’ve seen well-prepared businesses recover in days, while others spend months in a “coverage limbo” because they inadvertently violated their policy conditions within hours of the attack. Most business owners view their cyber policy as a rainy-day fund, but it’s actually a highly specific Service Contract. If you don’t follow the rules of the road from minute one, you aren’t just fighting a hacker, you’re fighting your own policy.

Here is what your cyber policy actually requires you to do in the first 24 hours.

1. The “Panel” Constraint: Don’t Call Your IT Guy (Yet)

This is the most common mistake we see. When a server goes down, the first instinct is to call your local IT provider or a favorite security consultant. Stop.

Almost every 2026 cyber policy contains a “Panel Provider” clause. This mandates that you must use the carrier’s pre-approved forensic investigators, legal counsel, and public relations firms. If you hire an outside firm without the carrier’s written consent, those costs—which can easily reach $500/hour—will likely be completely excluded from your claim.

2. The “Breach Coach” and the Shield of Privilege

Your policy typically requires you to notify their 24/7 Hotline immediately. This triggers the assignment of a Breach Coach (a specialized attorney).

In the first 24 hours, the Breach Coach is your most important asset. They don’t just manage the timeline; they establish Attorney-Client Privilege over the forensic investigation. If you investigate the breach yourself or with an unapproved IT team, those initial findings—including any “smoking gun” emails about your security flaws, could be discoverable in a future class-action lawsuit.

3. The “Don’t Touch” Rule: Preservation of Evidence

It is a human instinct to want to “fix” the problem immediately. However, your policy requires you to preserve evidence.

If your team wipes a server and restores from backup before a forensic image can be taken, you have essentially destroyed the “crime scene.” This can lead to a denial of claim because the carrier can no longer verify how the breach happened, what data was accessed, or if the threat actor is still hiding in your system.

The 24-Hour Checklist: Policy vs. Reality

To help you stay in compliance with your 2026 reporting requirements (including the new CIRCIA and NIS2 timelines), use this comparison:

| Priority | The Instinctive (Wrong) Move | The Policy-Compliant (Right) Move |

| Notification | Waiting until you know the “full story.” | Immediate notification of the carrier (even on a “suspected” breach). |

| Vendor Choice | Calling your long-term IT partner. | Calling the Policy Hotline to activate a Panel Breach Coach. |

| Containment | Reformatting affected servers immediately. | Isolating systems without destroying forensic logs or volatile memory. |

| Reporting | Thinking you have 30 days to report. | Reporting ransomware payments within 24 hours (per new 2026 regulations). |

| Evidence | Keeping internal “venting” emails about the hack. | Directing all communication through the Breach Coach for legal privilege. |

4. The 2026 Reporting Crunch

As of this year, the regulatory clock is ticking faster than ever. New federal and global mandates (like CIRCIA) now require “Significant Cyber Incidents” to be reported to authorities within 72 hours, and ransomware payments within a mere 24 hours.

Your insurance policy is designed to help you meet these deadlines, but the carrier can only help you if you bring them in at hour zero. If you spend the first day “trying to figure it out yourself,” you are already behind a clock that doesn’t pause for the weekend.

Take Control Before the “Golden Hour” Begins

The worst time to read your cyber policy is while your files are being encrypted. You need to know the name of your Breach Coach, the number for your Hotline, and the specific vendors on your Panel before the lights go out.

At Skyscraper Insurance, we believe that the best incident response isn’t a reaction—it’s a pre-tested strategy. We help our clients build “Incident Response Playbooks” that are specifically mapped to their actual policy language.

Is your team ready to perform under pressure? Don’t leave your 2026 resilience to chance. Reach out to our expert team today to schedule a comprehensive Incident response test. We will run a tabletop exercise for your leadership team, verify your “Panel” readiness, and ensure that when the “Golden Hour” strikes, your business is built to survive.

Skyscraper Insurance: We Share Your Vision for a Better Tomorrow!