In the HR and insurance world, a Professional Employer Organization (PEO) is often described as a “one-stop shop” for payroll, benefits, and workers’ compensation. For many growing firms, it’s a lifesaver. But for others, it becomes the insurance equivalent of “the golden handcuffs.”

You like the administrative ease, but you hate the lack of transparency when renewal season hits. At Skyscraper Insurance, we’ve found that the biggest mistake business owners make isn’t staying in a PEO, it’s staying in a PEO on the wrong timeline.

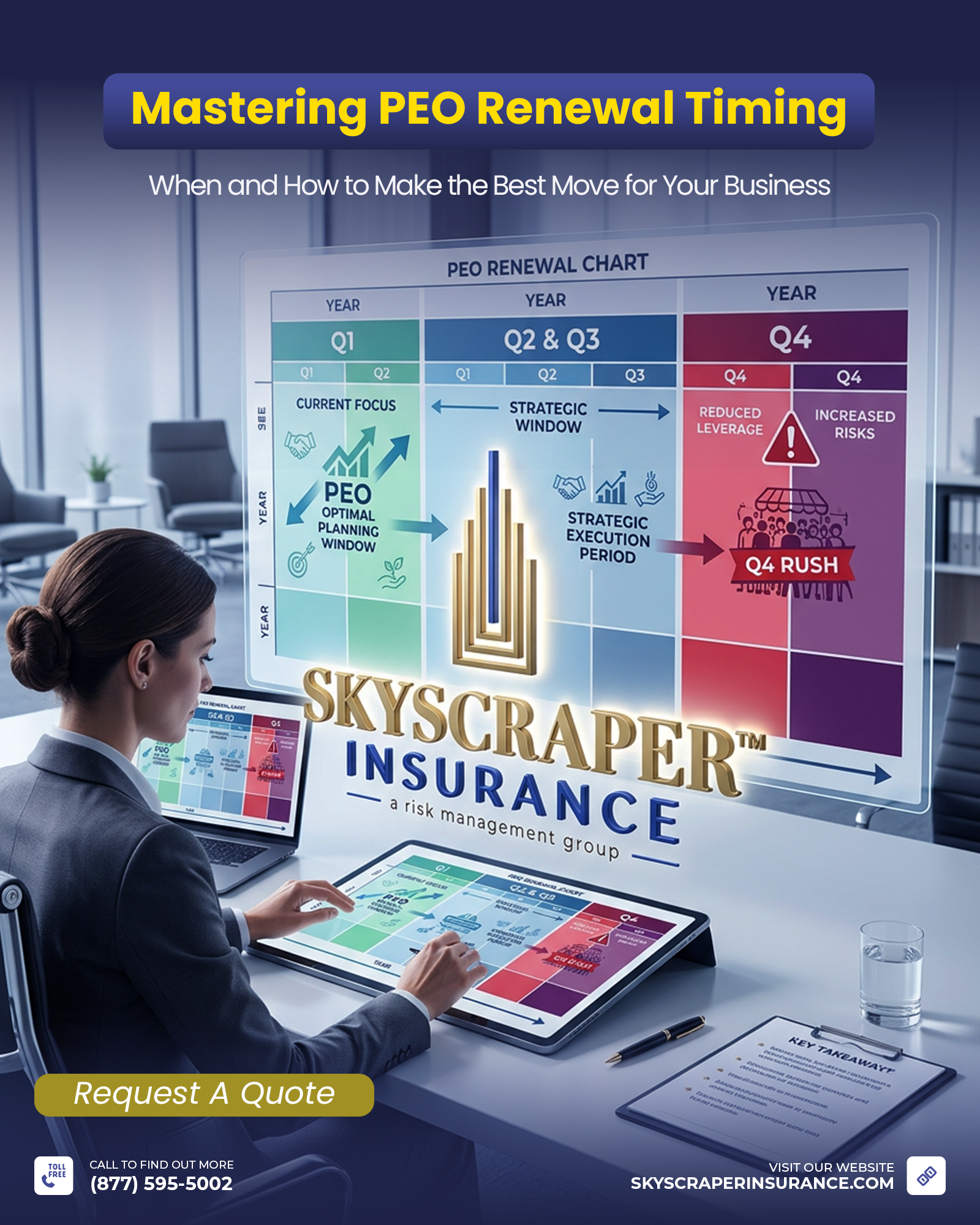

As we navigate the 2026 landscape, the strategy has shifted. If you wait for the PEO to send you a renewal notice to start looking at alternatives, you’ve already lost your leverage.

1. The “Master Policy” Bottleneck

Most PEOs operate on a Master Policy cycle, typically renewing their own coverage with carriers on January 1st or July 1st. When you are inside a PEO, your “individual” renewal is often tied to this massive collective date.

The problem? In Q4 (October through December), underwriters are buried in a mountain of submissions. If you try to move or renegotiate during the “January 1st Rush,” your business is just another number in a stack. By moving your evaluation to an Off-Cycle timing (Q2 or Q3), you gain the full attention of the market, often resulting in more aggressive pricing.

2. The E-Mod “Drop” Opportunity

For businesses with high-risk laborers, your Experience Modification Rate (E-Mod) is your most important financial metric.

If your E-Mod is set to drop mid-year due to improved safety results, staying in a PEO until their “standard” renewal date might mean you are overpaying for months.

The Math of the Switch:

If your current workers’ comp rate is $R$ and your E-Mod is dropping from $1.2$ to $0.9$, your cost per $\$100$ of payroll changes according to:

$$Modified\ Rate = R \times E\text{-}Mod$$

Waiting six months to capture that $0.3$ difference can cost a mid-sized company tens of thousands in unnecessary “admin load.”

3. Benefit “Plan-Year” Misalignment

One of the most effective ways to save money is to decouple your benefits renewal from your workers’ comp renewal. PEOs love to bundle these so you feel overwhelmed by the complexity of leaving.

However, if health insurance rates are spiking in 2026, switching to a carved-out benefits plan during a “soft” market window can stabilize your budget.

The Timing Matrix: Peak vs. Off-Peak Switching

To help you visualize when the market is most “hungry” for your business, review the timing table below:

| Timing Window | Market Condition | The “Switch” Advantage |

| Q4 (The Jan 1 Rush) | Saturated / Stressed | High inertia; PEOs hold the power. |

| Q1 (The Post-Jan Thaw) | Quiet / Selective | Carriers are looking to fill new yearly quotas. |

| Q2 (The Strategic Window) | Aggressive | Best time to audit E-Mod drops and “carve out” benefits. |

| Q3 (The Pre-Peak Prep) | Balanced | Good for businesses with July 1st fiscal starts. |

4. The “Administrative Thaw”: Is the PEO Still Scaling With You?

PEOs are priced on a per-head basis or a percentage of payroll. When you were 10 employees, that $Admin\ Fee$ was a bargain. Now that you are at 50 or 100 employees in 2026, the “efficiency” of the PEO model starts to invert.

If your headcount has grown by more than 20% this year, your current PEO is likely making a significant margin on your administrative fees. This is a primary “trigger” to look at a High-Deductible standalone plan or a Captive insurance model.

Stop Guessing. Start Timing.

The PEO model isn’t “broken,” but the way most businesses manage it is. Relying on the PEO’s internal timeline is a recipe for stagnant pricing and “take it or leave it” renewal increases.

At Skyscraper Insurance, we specialize in “PEO Arbitrage.” We look at your payroll data, your E-Mod projections, and the 2026 benefit trends to determine the exact moment your business should stay, negotiate, or go.

Is your PEO renewal date working against your bottom line? Don’t wait for the Q4 crunch to find out you’re overpaying. Reach out to our expert team today for a comprehensive PEO timing consult. We will audit your current fees, map your E-Mod trajectory, and ensure you have the leverage you need to protect your profit margins.